Land Development Opportunities in the East Midlands

With developed land under the UK average and the number of jobs greater than number of employees, the East Midlands represents a good long-term opportunity

Leaders Romans Group (LRG) has identified the East Midlands as one of the best opportunities for land investment in the UK. Working with its planning consultancy, Boyer, and its development economics team, LRG has drawn on extensive internal and external statistics which paint a very positive picture of investment opportunities in Nottingham and the surrounding area.

Land availability

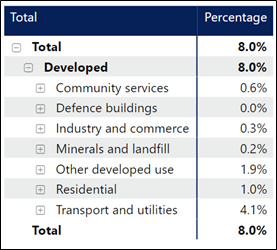

The first stage of the development process is land allocation and purchase. Government figures reveal that only 8.0% of land in the East Midlands is developed. This compares to a UK average of 8.7% - and is in stark contrast to a public perception that 47.1% of land is developed upon.

The remaining 92% is either agriculture, forestry, outdoor recreation, residential gardens or open land and water.

Perhaps even more significantly, much of this land is technically suitable for development: only 5% of land in the East Midlands is designated Green Belt (compared to 12.6% across England). In fact, according to Government statistics, the amount of land designated as Green Belt in Derby and Nottingham has dropped since 2013-14.

Population expansion in suburban areas

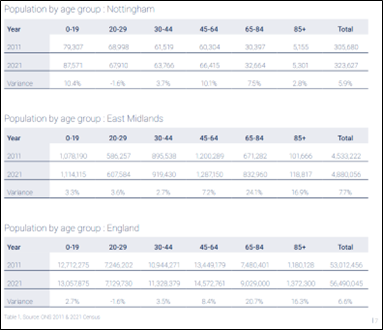

Given the land use figures, it is unsurprising that the population density by the number of persons per sq km in Nottingham and the East Midlands is lower than the national average. According the 2021 census, the population across the East Midlands was 312 per km2 (4,338 per km2 in Nottingham specifically). This compares to 434 per km2 for England as a whole.

Data from the last two censuses shows that the population of the East Midlands rose by 7.7% (above the national average of 6.6%), and 5.9% in Nottingham. This demonstrates a preference for rural / suburban living over urban, especially among older age groups.

Demand for housing

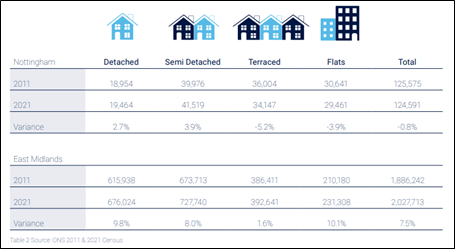

The next stage of the land investment process concerns the determination of housing need. The tables below use the census data to show the types of homes currently existing in Nottingham and the East Midlands and the ‘variance’ shows the change over a decade.

In 2021, there were 124,591 households within Nottingham. This represents 6.1% of the total number of households in the East Midlands (2,027,713 households). Over the ten year period, the number of households in Nottingham decreased from 125,575 in 2011 to 124,591 in 2021, a reduction of 0.8%. The East Midlands, on the other hand, saw the number of households grow by 7.5%. Again, this demonstrates the popularity new communities and urban extensions over infill sites in city centres.

Strong economic indicators

The economic circumstances within Nottingham and the East Midlands are also conducive to new development. Gross Value Added (GVA), a measure of an area’s contribution to the UK economy based on the value of the goods and services it produces per year, shows that the East Midlands contributed over £118 billion in the year 2021. Of this total, Nottingham contributed in excess of £10.7 billion.

Job density (the measure of the number of jobs in an area measured against the working population) is also positive. In fact, there is currently an over-supply of jobs for the size of the workforce: in 2021, Nottingham had a job density of 1.03 meaning that for 1,000 people there were 1,030 jobs. Major employees in Nottingham include the University of Nottingham, Experian, Capital One, Center Parcs, NHS, Boots and E-on.

Existing transport infrastructure

Good transport links are vital to the successful functioning of a new community, and the East Midlands benefits from an excellent road network (the M1, A1, M42, A52, A50 and A46) are easily accessible from Nottingham), a good train service (Derby in 31 minutes, Loughborough in 22 minutes and Leicester in 21 minutes); also access to both East Midlands Airport (13 miles) and Birmingham International (49 miles).

Commenting on the suitability of the East Midlands for development, LRG Land Director David Hutchinson says, “With significant amount of available land, few land use restrictions such as Green Belt and a growing population – but also a need for a larger population to fill the available jobs – the East Midlands is unsurprisingly proving very popular with residential developers.

“Already we have strategic landowner instructions covering greenfield land with a capacity to deliver in the region of 9,000 homes (resulting from 18 individual schemes). We also have a further four commercial opportunities with capacity to deliver in the region of 9 million square foot of roadside logistics.

“Furthermore, with the Government’s levelling up agenda prioritising the East Midlands, economic growth is set to continue, and so it is unsurprising that developers are already motivated to secure sites now.”